Smarter email, faster business.

Auto-tag, parse, and respond to RFQs, quotes, orders, and more — instantly.

Trending

Categories

Aviation News. Powered by AI.

Verified by ePlane AI

AI fact-checks every story before it goes live.

Latest News

Trending News

Rwanda Launches Africa’s First Autonomous Air Taxi Flight

Rwanda Launches Africa’s First Autonomous Air Taxi Flight

Rwanda has achieved a historic milestone by conducting Africa’s first public flight of a self-flying electric air taxi, the government announced on Wednesday. The demonstration, carried out in collaboration with the China Road and Bridge Corporation (CRBC), showcased the EHang EH216-S, a pilotless electric vertical takeoff and landing (eVTOL) aircraft. This event positions Rwanda as a leader in the advancement of air mobility technology on the continent.

Strategic Vision and Partnership

The Ministry of Infrastructure highlighted that this initiative forms part of Rwanda’s broader ambition to establish itself as a hub for testing and deploying innovative aviation technologies. By leveraging CRBC’s global engineering expertise, Rwanda aims to cultivate a new ecosystem for advanced air mobility. The government envisions this technology as a means to alleviate urban traffic congestion, enhance connectivity to remote areas, and promote environmentally sustainable transportation solutions.

Infrastructure Minister Jimmy Gasore underscored the significance of the partnership with CRBC, stating that it provides a solid foundation for introducing cutting-edge technologies and expertise to Rwanda. He emphasized that the historic flight not only demonstrates the future potential of aviation but also reflects the country’s commitment to developing a safe and progressive regulatory framework for advanced air mobility.

Event and Future Challenges

The EHang EH216-S demonstration took place during the African Aviation Summit in Kigali, Rwanda’s capital, attracting investors and stakeholders interested in the rapidly evolving sector of advanced air mobility. While the successful flight marks a significant achievement, Rwanda faces several challenges in scaling the adoption of autonomous air taxis. These include the development of comprehensive regulatory frameworks, the management of increasingly complex airspace, and the establishment of a network of vertiports to support eVTOL operations. Addressing these challenges will require coordinated efforts among government bodies, industry partners, and international regulatory authorities.

The success of Rwanda’s autonomous air taxi flight is expected to stimulate greater interest and investment in Africa’s advanced air mobility market. It may also prompt competitors, such as Joby Aviation—which has already completed piloted eVTOL flights between U.S. airports—to accelerate their own projects in response to Rwanda’s progress.

As Rwanda continues to pioneer advanced air mobility on the continent, its experience may serve as a valuable model for other nations seeking to integrate autonomous aviation technologies into their transportation infrastructure.

GE Aerospace and BETA Technologies Collaborate on Hybrid Electric Aviation

GE Aerospace and BETA Technologies Collaborate to Advance Hybrid Electric Aviation

In a significant development within the rapidly evolving Advanced Air Mobility (AAM) sector, GE Aerospace and BETA Technologies have announced a strategic partnership aimed at accelerating the commercialization of hybrid electric aviation. This alliance combines GE’s extensive expertise in turbine technology and certification processes with BETA’s innovative electric propulsion systems. Together, they seek to address the limitations inherent in battery-only aircraft and respond to the increasing global demand for sustainable, high-performance aviation solutions.

Strategic Investment and Industry Implications

GE Aerospace has committed $300 million in equity investment to BETA Technologies, securing a seat on the company’s board and underscoring a long-term strategic alignment. This substantial financial commitment is intended to capitalize on BETA’s capabilities in electric generators and flight testing, while leveraging GE’s mastery of turbine systems and regulatory certification. Central to the partnership is the development of a hybrid electric turbogenerator derived from GE’s CT7 and T700 engines. This system is projected to enhance performance metrics significantly, offering up to 30% greater range, 20% higher payload capacity, and 15% faster speeds compared to existing electric vertical takeoff and landing (eVTOL) platforms.

The hybrid approach directly addresses a critical challenge in AAM: the need for scalable aircraft capable of reliable operation across diverse conditions and compatibility with current infrastructure. By integrating proven turbine technology with electric propulsion, GE and BETA position themselves at the forefront of the industry’s transitional phase toward full electrification. Market analysts have responded favorably, interpreting GE’s investment as a strategic move to lead in hybrid-electric technology. This partnership is expected to reshape the trajectory of hybrid electric aviation, compelling competitors to accelerate their own hybrid development efforts to maintain competitiveness in a swiftly evolving market.

Regulatory Progress and Certification Milestones

Regulatory challenges have historically impeded the adoption of electric aviation technologies. However, recent developments suggest a more conducive environment for innovation. In December 2024, the Federal Aviation Administration (FAA) issued final Special Conditions for BETA’s pusher electric engine, marking a critical step toward certification. This move reflects the FAA’s evolving approach toward performance-based regulations, which allow manufacturers to propose customized compliance methods.

Additional progress includes Hartzell Propellers’ certification of a five-bladed electric propeller designed for BETA’s Alia CX300 and Alia 250 eVTOL models, facilitating a smoother path to commercialization. GE Aerospace’s prior achievements, such as the 2022 test of a megawatt-class hybrid system operating at 45,000 feet, have demonstrated the practical feasibility of integrating electric and turbine components under commercial flight conditions. These milestones position the GE-BETA collaboration to secure FAA certification for its hybrid turbogenerator by 2026, aligning with BETA’s certification targets for the Alia CX300 in 2025 and the Alia 250 eVTOL in 2026.

Competitive Advantages and Market Outlook

While competitors such as Joby Aviation and Archer Aviation focus primarily on pure-electric eVTOL designs, GE and BETA’s hybrid system offers a pragmatic balance between performance and operational practicality. For instance, Joby’s air taxi, anticipated to enter service by 2030, relies exclusively on battery power and is limited to a range of under 150 miles per charge. In contrast, the GE-BETA hybrid system extends operational range beyond 300 miles, making it suitable for regional freight and passenger transport.

The global electric aircraft market is projected to grow at a compound annual growth rate of 20%, reaching an estimated $71 billion by 2034. Within this expanding market, hybrid systems that effectively balance energy density with infrastructure compatibility are expected to play a pivotal role. The partnership between GE Aerospace and BETA Technologies is well positioned to lead this transition, setting new benchmarks for the future of sustainable aviation.

Electric Aircraft Startup Vaeridion Acquires Specialized Facility from Lilium

Electric Aircraft Startup Vaeridion Acquires Specialized Facility from Lilium

Electric aircraft startup Vaeridion has secured a lease and is poised to acquire a specialized facility from Lilium, the German eVTOL developer currently navigating insolvency proceedings, according to a report by *Wirtschaftswoche*. Vaeridion’s founder and CEO, Ivor van Dartel, confirmed that the company obtained approval from Lilium’s insolvency administrator to purchase critical technology housed at the site, including advanced laser welding equipment essential for aircraft manufacturing.

Distinct Approaches in Electric Aviation

While Lilium has concentrated on electric vertical take-off and landing (eVTOL) air taxis, Vaeridion is developing a conventional electric aircraft designed for runway operations. The startup’s planned model will accommodate nine passengers alongside two pilots, offering an estimated range exceeding 400 kilometers with an emergency reserve. To support this ambitious project, Vaeridion successfully raised €14 million from investors in December.

The facility, situated at Oberpfaffenhofen Airport, holds particular strategic value for Vaeridion due to its fireproof room, a critical feature for safe battery production. Additionally, the site includes halls equipped for acoustic testing, originally constructed to meet Lilium’s development requirements. As Lilium shifts its business model, it aims to lease such specialized facilities to other companies within the electric mobility sector, promoting a “testing-as-a-service” approach.

Uncertainty Surrounding Lilium’s Future and Industry Challenges

Vaeridion’s acquisition occurs amid ongoing uncertainty about Lilium’s future. The proposed takeover of Lilium by Advanced Air Mobility Group (AAMG) remains unapproved by insolvency administrator Ivo-Meinert Willrodt of the Pluta law firm. Willrodt has expressed reservations about AAMG, a newcomer to the aviation industry whose CEO, Robert Kamp, has openly acknowledged his limited experience in the sector. Despite AAMG’s public commitment to continue research and development in Bavaria with a reduced workforce and plans to produce the first 50 air taxis locally before transferring series production to Japan, the administrator has yet to endorse the deal. This cautious stance follows a previous failed takeover attempt by Mobile Uplift Corporation, which culminated in Lilium’s second insolvency.

The transfer of the facility to Vaeridion also underscores broader challenges facing the electric aviation sector. Lilium’s incomplete development program and persistent certification hurdles have intensified skepticism within the industry regarding the viability of electric aircraft. Market participants remain cautious, closely monitoring regulatory progress and the ability of startups to fulfill their ambitious objectives. In response, rival companies are likely to accelerate efforts to secure regulatory approvals and expand their footprint in the emerging advanced air mobility market.

Meanwhile, Vaeridion has already onboarded eleven former Lilium engineers and plans further recruitment, signaling a strong commitment to advancing its electric aircraft program. Establishing a comparable facility independently would likely require approximately one year, highlighting the strategic importance of this acquisition as Vaeridion seeks to establish itself in a competitive and rapidly evolving industry.

How the Boeing 777-300ER Compares to the Airbus A380 in Size

How the Boeing 777-300ER Compares to the Airbus A380 in Size

When discussing the largest commercial aircraft in operation today, the Boeing 777-300ER and the Airbus A380 are the two dominant models. Each represents a significant achievement in aerospace engineering but caters to different operational needs and market demands. Their differences in size, passenger capacity, and intended use highlight the distinct roles they play within global aviation.

Size and Capacity: A Detailed Comparison

The Airbus A380 holds the distinction of being the largest passenger airliner ever constructed. Its unique double-deck design enables it to accommodate up to 853 passengers in an all-economy configuration, or approximately 575 passengers in a more typical three-class layout. By contrast, the Boeing 777-300ER, the largest variant within the 777 family, can seat a maximum of 550 passengers in a high-density arrangement, though it more commonly carries around 396 passengers in a three-class configuration.

Physically, the A380 exceeds the 777-300ER in nearly every dimension except length. The 777-300ER measures 242 feet 4 inches (73.9 meters) in length, slightly longer than the A380’s 238 feet 7 inches (72.7 meters). However, the A380’s wingspan extends to 261 feet 8 inches (79.8 meters), significantly wider than the 777-300ER’s 212 feet 7 inches (64.8 meters). The A380 also stands taller at 79 feet (24.1 meters), compared to the 777-300ER’s height of 61 feet (18.5 meters). In terms of maximum takeoff weight, the A380’s 1,234,600 pounds (560,000 kilograms) far surpasses the 777-300ER’s 775,000 pounds (351,534 kilograms). These dimensions underscore the A380’s dominance in size and capacity, despite the 777-300ER’s advantage in length.

Operational Roles and Market Positioning

The Boeing 777-300ER was engineered to serve long-haul routes with a focus on operational efficiency and flexibility. Its twin-engine design allows it to operate from a broader range of airports, including those unable to accommodate the larger A380. This versatility, combined with lower operating costs and a moderate passenger capacity, makes the 777-300ER a preferred choice for airlines seeking to balance capacity with economic performance.

Conversely, the Airbus A380 was developed to maximize passenger volume on high-density international routes, primarily connecting major global hubs. Its immense size necessitates specialized airport infrastructure, limiting the number of airports capable of handling the aircraft. Nevertheless, the A380 remains a favored option for carriers aiming to transport large numbers of passengers efficiently on heavily trafficked routes.

Industry Response and Future Developments

The market’s response to these aircraft reflects their strategic roles within the aviation sector. Emirates, the largest operator of the A380, continues to invest in the superjumbo, with plans to upgrade its first-class suites and extend the aircraft’s operational lifespan through 2040. The airline has also expressed interest in Boeing’s developments, including visits to Boeing’s assembly facilities to monitor progress.

Meanwhile, other airlines are reassessing their fleet compositions. Kenya Airways, for example, is considering reintroducing the 777-300ER alongside exploring the Boeing 737 MAX, demonstrating the ongoing relevance of the 777 family. In response to Boeing’s advancements, Airbus is developing a stretched version of its A350 to compete directly with the forthcoming Boeing 777-9, highlighting the competitive dynamics shaping the large aircraft market.

Conclusion

While the Airbus A380 remains the world’s largest passenger aircraft by nearly every measure except length, the Boeing 777-300ER continues to hold a vital position in commercial aviation due to its versatility and efficiency. Both aircraft exemplify the evolving demands of the industry and maintain prominent roles in the global air travel landscape.

Air India Announces Delivery Schedule for A321neo, A350-1000, and 787-9 Aircraft

Air India Announces Delivery Schedule for A321neo, A350-1000, and 787-9 Aircraft

Major Fleet Modernization Underway

Air India Group, now under the ownership of the Tata Group, is advancing a landmark fleet renewal initiative that promises to transform its operational capabilities and competitive positioning within the Indian aviation sector. Central to this effort is an unprecedented order of 570 aircraft, among the largest in the history of commercial aviation. This extensive acquisition includes the latest models from Airbus and Boeing, notably the A321neo, A350-1000, 787-9 Dreamliner, and 777-9. These additions are expected to significantly expand Air India’s capacity and modernize its fleet.

Delivery Timeline and Deployment Plans

To date, the Air India Group—which comprises both Air India (AI) and Air India Express (IX)—has taken delivery of six Airbus A350-900s alongside more than 40 Boeing 737 MAX aircraft. The next phase of this fleet expansion is scheduled to commence in mid-2025, with the introduction of the first A321neo, A350-1000, and 787-9 Dreamliner aircraft. This phase represents a critical step in the airline’s strategy to increase capacity and enhance service offerings.

Air India Express will be the initial operator of the new A321neo, launching scheduled services from April 15, 2025. The inaugural routes will connect Delhi (DEL) with Bengaluru (BLR) and Srinagar (SXR), with subsequent expansions on April 20 to include Ayodhya (AYJ) and Jaipur (JAI). The A321neo will be configured with 180 economy seats and 12 business class seats, providing improved passenger options on key domestic routes. Currently, Air India operates two A321neos (registrations VT-RTC and VT-RTD) in a 192-seat dual-class layout.

Supply Chain Challenges and Operational Adjustments

Despite the progress, Air India continues to grapple with significant supply chain disruptions. CEO Campbell Wilson has acknowledged ongoing difficulties in procuring essential components such as engines, fuselages, and premium cabin seats. These challenges are expected to cause delivery delays from both Airbus and Boeing, potentially affecting the airline’s growth trajectory for the next four to five years. In response, Air India is extending the operational lifespan of older aircraft, which entails increased maintenance costs, and is facing obstacles in leasing additional planes due to global shortages. The airline is also exercising prudence regarding further Boeing orders amid manufacturing and regulatory constraints.

Widebody Fleet Expansion: A350-1000 and 787-9

The first A350-1000 destined for Air India is nearing completion at Airbus’s Toulouse facility and is anticipated to be delivered in 2026. Currently registered as F-WZFI, the aircraft will soon be re-registered under the VT-series for Indian operations. Concurrently, the initial Boeing 787-9 Dreamliners from the 2023 order are expected to arrive by the end of 2025. Three 787-9s are presently in production at Boeing’s Charleston, South Carolina plant, equipped with General Electric GEnx-1B engines.

Order Composition and Market Implications

Air India’s comprehensive 570-aircraft order includes 20 A350-900s, 20 A350-1000s, 140 A320neos, and 70 A321neos from Airbus, alongside 20 787-9 Dreamliners, 10 777X, and 190 737-8 MAX aircraft from Boeing. Additionally, a 2024 order comprises 10 more A350s and 90 A320 Family aircraft. This sweeping modernization is anticipated to provoke strategic responses from rival carriers, who may reassess their fleet plans in light of Air India’s expanded capacity. Industry analysts expect this development to intensify competition and elevate passenger service standards across the Indian aviation market.

Commitment to Sustainability and Efficiency

Air India’s investment in next-generation aircraft reflects a strong commitment to operational efficiency, passenger comfort, and environmental stewardship. The new A350 and 787-9 models offer substantial fuel savings and reduced emissions, aligning with global efforts to promote sustainable aviation. As these aircraft enter service from mid-2025 onward, Air India is positioned to lead the industry’s transition toward eco-friendly, high-capacity air travel.

Finnair to Renew Narrowbody Fleet with Order of Up to 30 Airbus Jets

Finnair Plans Significant Narrowbody Fleet Renewal with Potential Airbus Order

Finnair is poised to undertake a major renewal of its short-haul fleet, with plans to acquire up to 30 new Airbus narrowbody aircraft, according to CEO Turkka Kuusisto. Speaking on September 3, Kuusisto indicated that while the immediate need might be for around 15 aircraft, a broader analysis suggests the requirement could extend to 25 or even 30 jets. The Finnish flag carrier currently operates a fleet of 80 aircraft, but approximately 15 of its older narrowbody planes are approaching retirement, making their replacement a pressing priority.

Strategic Importance of Fleet Modernization

Although Finnair has yet to finalize the specific aircraft model, a decision is anticipated by the end of the year. The airline’s network, which serves as a critical link between Europe and Asia via its Helsinki hub, depends heavily on narrowbody jets for regional and intra-European routes. Modernizing this segment is expected to yield multiple benefits, including reduced emissions, lower operating costs, and improved operational efficiency.

The timing of this potential order coincides with Airbus’s dominant position in the global narrowbody market. The Airbus A320 family accounted for more than 56% of combined commercial utilization in 2019, and Airbus is on track to surpass Boeing in narrowbody deliveries, further consolidating its market leadership. Finnair’s move may prompt competitors to accelerate their own fleet renewal programs or consider alternative aircraft to maintain competitiveness.

Industry Context and Financial Considerations

Industry analysts highlight that Finnair’s decision will likely attract close attention regarding the airline’s financial health and operational performance, especially as the aviation sector increasingly prioritizes newer, more fuel-efficient aircraft. The advent of long-range narrowbody models is also influencing airline strategies by enabling expanded route networks and greater operational flexibility—factors that are expected to weigh heavily in Finnair’s final aircraft selection.

Current Fleet Composition

As of 2025, Finnair’s fleet comprises a diverse mix of aircraft, including 12 ATR 72s with an average age of 16.3 years, five Airbus A319s averaging 24.3 years, 10 Airbus A320s at 23.2 years, and 15 Airbus A321s averaging 11.1 years. The long-haul fleet includes eight Airbus A330-300s (16 years average age) and 18 Airbus A350-900s (7.6 years average age), alongside 12 Embraer E190s averaging 17.3 years. The aging narrowbody aircraft, particularly the A319s and A320s, underscore the urgency of the planned renewal.

As the airline industry continues its transition toward more sustainable and cost-effective fleets, Finnair’s anticipated order is set to play a crucial role in shaping its future operations and competitive position within the European market.

Cathie Wood’s ARK Invest Increases Stake in Archer Aviation as Air Taxis Advance

Cathie Wood’s ARK Invest Increases Stake in Archer Aviation as Air Taxis Advance

Cathie Wood’s ARK Invest has significantly expanded its investment in Archer Aviation, underscoring its confidence in the burgeoning urban air mobility sector. As electric air taxis move closer to commercial deployment, ARK has increased its holdings in Archer through three of its thematic exchange-traded funds (ETFs): ARK Space Exploration & Innovation (ARKX), ARK Autonomous Technology & Robotics (ARKQ), and the flagship ARK Innovation (ARKK). Archer, a leading developer of electric vertical takeoff and landing (eVTOL) aircraft, has become a focal point for ARK’s strategy of early exposure to transformative technologies.

Strategic Positioning Across Multiple Funds

ARK’s approach involves diversifying risk by allocating positions in Archer across several funds with distinct thematic focuses. ARKX, which concentrates on aerospace and satellite technologies, holds a 5.3% stake in Archer alongside investments in orbital and defense companies. ARKQ, dedicated to automation and robotics, assigns a 4.8% weighting to Archer. Meanwhile, ARKK, ARK’s core innovation fund, includes Archer within a broader portfolio spanning genomics, fintech, and artificial intelligence sectors. This multi-fund strategy enables investors to engage with the urban air mobility trend while mitigating the volatility inherent in a single stock.

The timing of ARK’s increased investment coincides with key milestones for Archer. The company recently completed its longest test flight, covering 55 miles in 31 minutes, marking significant progress toward Federal Aviation Administration (FAA) certification expected in 2026. Archer is advancing production with three Midnight eVTOL aircraft in final assembly and has bolstered its position through two defense-related acquisitions. Supported by prominent partners such as United Airlines, Stellantis, and defense contractor Anduril, and backed by a $6 billion order book, Archer is emerging as a frontrunner in the race to commercialize air taxis.

The Emerging Market for Urban Air Mobility

Major metropolitan areas in the United States, including Los Angeles, Miami, New York, and San Francisco, are anticipated to be among the first to introduce commercial air taxi services. Internationally, Abu Dhabi plans to launch an initial network by 2025. Archer’s flagship Midnight aircraft, designed to carry four passengers and a pilot for distances up to 100 miles, aims to revolutionize urban commuting by reducing travel times dramatically—for example, cutting a 45-minute drive between downtown Los Angeles and LAX airport to a 10-minute flight.

Despite the promising outlook, the sector faces considerable challenges. Regulatory approval processes remain complex, technological hurdles persist, and competition is intensifying. Key rivals such as Joby Aviation, Boeing’s Wisk Aero, and Hyundai’s Supernal are all competing for leadership in the advanced air mobility market. ARK’s increased commitment to Archer reflects its belief in the company’s potential for outsized returns, though the broader market will be closely monitoring upcoming regulatory and technical developments.

For investors interested in the air taxi revolution, ARK’s ETFs provide a diversified and risk-managed avenue to participate in this rapidly evolving industry, offering exposure to the future of urban flight without reliance on a single eVTOL manufacturer.

Aviation Expert Richard Godfrey Attributes AI 171 Crash to RAT Deployment, Rules Out Pilot Error

Aviation Expert Richard Godfrey Attributes AI 171 Crash to RAT Deployment, Rules Out Pilot Error

Aviation expert Richard Godfrey has identified the automatic deployment of the Ram Air Turbine (RAT) as the primary cause of the Air India Flight 171 crash in Ahmedabad on June 12, dismissing widespread speculation that pilot error was to blame. In an interview with Geoffrey Thomas, Godfrey examined preliminary findings and data released by the Air Accident Investigation Bureau (AAIB) a month after the London-bound aircraft crashed, resulting in the deaths of all but one passenger.

Timeline and Key Findings

The AAIB’s preliminary report outlines a rapid sequence of events on the day of the crash. At 1:13 pm, the aircraft requested pushback and startup clearance, followed by Air Traffic Control (ATC) confirming the need for the full length of Runway 23 at 1:19 pm. Taxi clearance was granted at 1:25 pm, and by 1:33 pm, AI 171 was instructed to line up for takeoff. The flight was cleared for takeoff at 1:37 pm, but just two minutes after liftoff, the pilots issued a MAYDAY call before the aircraft crashed seconds later.

The report highlights that both engines shut down within one second of each other after the fuel supply was cut off. Cockpit voice recordings captured one pilot questioning the other about the engine shutdown, with the second pilot denying any action to cut the engines. Examination of the engines recovered from the crash site revealed they were in the “Run” position, and attempts had been made to relight them.

RAT Deployment and Technical Analysis

Godfrey’s detailed analysis, drawing on the preliminary report, flight data, and airport CCTV footage, revealed that the RAT was automatically deployed at approximately 1:38:47 pm. According to the data, both engines’ N2 values dropped below minimum idle speed at this time, triggering the RAT hydraulic pump to supply hydraulic power. The preliminary report included an image showing the RAT in its extended position but did not clarify the timing or cause of its deployment.

By synchronizing multiple data sources—including the flight data recorder (FDR) and ATC logs—Godfrey established that the RAT deployment occurred mere seconds before the crash. This timing strongly suggests a technical malfunction rather than any human intervention.

Conflicting Interpretations and Ongoing Investigation

Despite Godfrey’s findings, the investigation has been marked by conflicting interpretations. Some experts, including Captain Byron Bailey, have proposed the possibility of deliberate pilot action, even suggesting “suicide by the pilot” as a theory. However, Godfrey’s analysis, supported by the available data, firmly disputes this notion, attributing the crash to a technical failure centered on the RAT deployment.

In response to the incident, the U.S. Federal Aviation Administration (FAA) and Boeing reviewed the safety of fuel cutoff switch locks, which had come under scrutiny during the investigation. Both organizations have since affirmed the safety of these components.

The investigation into the AI 171 crash remains ongoing, with authorities yet to issue a definitive conclusion. For now, Godfrey’s assessment shifts the focus away from pilot error, underscoring the critical role of the RAT deployment in the tragic sequence of events.

Air Lease Acquired in $7.4 Billion Deal Shrinking Airplane Leasing Market

Air Lease Acquisition Marks Major Shift in Aircraft Leasing Industry

Air Lease Corporation, a prominent Los Angeles-based aircraft leasing company founded by industry veteran Steven Udvar-Házy, has agreed to be acquired in a $7.4 billion deal by a consortium led by Japan’s Sumitomo Corporation and SMBC Aviation Capital, alongside asset managers Apollo Global Management and Brookfield Asset Management. Announced on Tuesday, the transaction will take Air Lease private and represents a significant move toward further consolidation within the global aircraft leasing sector.

Details of the Acquisition and Market Impact

Under the terms of the agreement, Air Lease shareholders will receive $65 per share, reflecting an 8% premium over the company’s closing price last Friday. When including debt, the total valuation of Air Lease reaches approximately $28.2 billion. The acquisition is expected to finalize by the end of 2026, with the newly formed entity, Sumisho Air Lease, to be headquartered in Dublin.

Aircraft lessors such as Air Lease play a vital role in the aviation industry by providing airlines with leased aircraft, allowing carriers to preserve capital rather than purchasing planes outright. This is particularly significant given that new commercial jets can exceed $100 million in list price. The sector has recently experienced a surge in rental rates, driven by a shortage of available aircraft caused by pandemic-related disruptions and ongoing supply chain challenges.

According to aviation consultancy IBA Group, aircraft lessors now control 58% of the world’s passenger jet fleet, up from 51% in 2009. However, growth in the sector has moderated as some major airlines have regained profitability and begun purchasing more aircraft directly. Stuart Hatcher, chief economist at IBA Group, noted, “Cash is not alien to these guys anymore,” highlighting airlines’ improved financial positions.

Industry Challenges and Future Outlook

Despite these gains, airlines are currently reevaluating their capacity strategies amid an oversupply of flights, which has exerted downward pressure on fares and profitability. Spirit Airlines, for instance, recently filed for Chapter 11 bankruptcy protection for the second time within a year, citing elevated costs and weakened demand as key factors.

The acquisition of Air Lease is poised to reshape the competitive landscape of aircraft leasing. The combined company, Sumisho Air Lease, will command a larger fleet and enhanced financial resources, potentially establishing dominance in critical market segments. This increased scale may attract regulatory scrutiny and compel competitors to adjust their strategies, including renegotiating lease agreements or pursuing new partnerships to sustain their market positions.

At the end of the second quarter, Air Lease owned 495 aircraft and, including its backlog, ranked as the world’s fifth-largest aircraft lessor, according to IBA. The deal exemplifies a broader trend of consolidation within the industry, as firms seek to grow their scale and influence. Hatcher remarked, “It makes perfect sense when you consider it’s … the cheapest way to buy market growth.”

As the transaction progresses toward completion, industry analysts and regulators will closely monitor the evolving competitive dynamics and potential regulatory responses that could further transform the global aircraft leasing market.

Canada achieves world-first piloted hydrogen-powered helicopter flight

Canada Achieves World-First Piloted Hydrogen-Powered Helicopter Flight

In a groundbreaking advancement for sustainable aviation, Canada has successfully completed the world’s first piloted flight of a hydrogen-powered helicopter. This milestone marks a significant step forward in the pursuit of zero-emission aircraft and highlights the country’s commitment to innovation in clean energy technologies.

Pioneering Sustainable Aviation

The historic flight took place with a modified helicopter equipped with a hydrogen fuel cell system, replacing traditional fossil fuel engines. The pilot-operated aircraft demonstrated the viability of hydrogen as a clean energy source for rotary-wing aviation, offering a promising alternative to conventional aviation fuels that contribute to greenhouse gas emissions.

This achievement not only showcases Canada’s technological capabilities but also aligns with global efforts to reduce the environmental impact of air travel. Hydrogen fuel cells produce electricity through a chemical reaction between hydrogen and oxygen, emitting only water vapor as a byproduct, thereby eliminating carbon emissions during operation.

Implications for the Future of Flight

The successful piloted flight opens new avenues for the development of hydrogen-powered aircraft, which could revolutionize the aviation industry by significantly lowering its carbon footprint. While challenges remain in scaling the technology and establishing the necessary infrastructure for widespread adoption, this demonstration provides a crucial proof of concept.

Canada’s accomplishment is expected to inspire further research and investment in hydrogen propulsion systems, potentially accelerating the transition toward more sustainable modes of air transportation worldwide. As the aviation sector seeks to meet increasingly stringent environmental regulations, innovations such as this will be vital in shaping the future of flight.

GKN Aerospace Expands Additive Manufacturing Operations in the US

GKN Aerospace Expands Additive Manufacturing Operations in Connecticut

GKN Aerospace is advancing its manufacturing capabilities in the United States with a significant expansion of its Newington, Connecticut facility. The company is establishing a new production line dedicated to the additive manufacturing of the fan case mount ring (FCMR), a vital component for Pratt & Whitney’s geared turbofan (GTF) engine, which powers aircraft such as the Airbus A220 and Embraer E195-E2. This expansion is anticipated to generate new employment opportunities and strengthen GKN Aerospace’s presence in the US aerospace sector.

Scaling Production and Technological Innovation

The FCMR program represents the largest flight-critical additive component to have received Federal Aviation Administration (FAA) certification, with full serial production expected by the end of 2025. Currently, the core structure of the component, known as the additively manufactured “hot size ring,” is produced at GKN Aerospace’s facility in Trollhättan, Sweden, with final machining performed in Newington. The Connecticut expansion will facilitate a significant increase in production capacity to meet rising market demand.

GKN Aerospace employs a proprietary additive manufacturing process that reduces material consumption, shortens production lead times, and achieves over 70% material savings. This innovative approach not only enhances manufacturing efficiency but also contributes to supply chain resilience by providing an alternative production method amid ongoing industry challenges.

Joakim Andersson, President of Engines at GKN Aerospace, emphasized the strategic importance of the expansion, highlighting the combination of local support, skilled workforce, and aerospace infrastructure as key enablers for scaling additive fabrication technology to industrial levels. Andersson noted that the initiative supports job creation and reinforces the company’s long-term partnership with Pratt & Whitney, while delivering tangible benefits in sustainability, lead times, and production predictability.

Sébastien Aknouche, Senior Vice President of Material Solutions at GKN Aerospace, added that the company currently produces approximately 30 FCMR units per month in Sweden. The transfer and expansion of this advanced technology to the US will consolidate full-volume production in one location and enable the company to broaden its additive manufacturing offerings to additional customers within the American market.

Challenges and Industry Implications

Despite the promising outlook, GKN Aerospace faces several challenges in scaling its US operations. These include navigating complex regulatory requirements, integrating advanced additive manufacturing technologies with existing production systems, and managing evolving supply chain logistics. Successfully addressing these factors will be critical to maintaining quality standards and operational efficiency.

Industry analysts suggest that GKN Aerospace’s investment may stimulate increased interest among investors in aerospace companies leveraging additive manufacturing technologies. Competitors such as GE Aerospace and Toyota are expected to intensify their efforts in this domain, potentially accelerating strategic investments and partnerships with technology providers like Stratasys.

GKN Aerospace currently operates two facilities in Connecticut—Newington and Cromwell—employing over 450 people statewide. This latest expansion follows a US$50 million investment announced in 2024 aimed at advancing sustainable additive manufacturing for both civil and military engine platforms, underscoring the company’s commitment to innovation and customer service.

ANA and Joby Aviation Demonstrate eVTOL Flights at Expo 2025 Osaka

ANA and Joby Aviation to Showcase eVTOL Flights at Expo 2025 Osaka

ANA Holdings (ANA HD) and Joby Aviation are preparing to demonstrate the future of urban air mobility at Expo 2025 Osaka, Kansai, Japan. From October 1 to 13, 2025, the two companies will conduct public flight demonstrations featuring the Joby S4 electric vertical takeoff and landing (eVTOL) aircraft. The Joby S4, adorned with a distinctive ANA livery, will provide visitors with a direct experience of the potential offered by electric air taxis.

The Joby S4: A New Era in Urban Aviation

The Joby S4 represents a significant advancement in eVTOL technology. This fully electric aircraft, with a wingspan of approximately 14 meters and a length of 7.6 meters, is designed to operate without the need for traditional runways, making it ideally suited for congested urban environments. Its quiet, zero-emission operation aligns with ANA’s broader commitment to sustainable travel solutions, positioning the S4 as a promising alternative to conventional aviation methods.

Public Demonstration Flights and Viewing Opportunities

The demonstration flights will originate from the EXPO Vertiport located within the Mobility Experience area of the Expo site. Two flights are scheduled daily at 11 a.m. and 2 p.m., with the possibility of additional flights on Saturdays at 4 p.m. Each flight will last between 10 and 15 minutes, showcasing the aircraft’s capabilities in vertical takeoff, wing-borne flight, and vertical landing. On October 3 and 8, the flights will pause to allow for special public exhibitions of the aircraft at the Vertiport hangar.

For attendees unable to secure a place on the demonstration flights, the eVTOL will be visible from several outdoor viewing areas, including the Grand Ring situated in front of the West entrance, offering ample opportunity to observe the aircraft in operation.

Industry Context and Future Prospects

The collaboration between ANA and Joby Aviation at Expo 2025 arrives amid growing global interest and investment in eVTOL technology. These demonstrations underscore the potential for faster, quieter, and cleaner urban transportation. Nevertheless, the sector faces considerable challenges, including regulatory approval processes, safety concerns, and technological limitations that must be addressed before widespread adoption can occur.

Market responses to eVTOL advancements have been mixed, with investor enthusiasm tempered by skepticism about the long-term viability of such operations. As ANA and Joby Aviation advance their partnership, competitors are expected to escalate research and development efforts and seek strategic alliances to maintain a competitive position in this emerging market.

While the Expo 2025 showcase marks a significant milestone toward the commercialization of eVTOL technology, integrating electric air taxis into daily urban life remains a complex endeavor. The event in Osaka will not only highlight technological progress but also emphasize the challenges that lie ahead for the sector.

As global attention focuses on Japan for Expo 2025, the ANA and Joby Aviation collaboration offers a revealing glimpse into the evolving landscape of sustainable urban mobility and the obstacles that must be overcome to realize its full potential.

Jetson Completes First Global Delivery with Palmer Luckey

Jetson Completes First Global Delivery with Palmer Luckey

A Milestone in Personal Aviation

Jetson, a pioneering company in personal aviation, has marked a significant milestone by completing its first global delivery of the Jetson ONE aircraft. The recipient, Palmer Luckey, a prominent entrepreneur and defense technology innovator, took delivery of the aircraft in Carlsbad, California. Luckey, widely recognized as the founder of Oculus and Anduril Industries, received the Jetson ONE at a dedicated facility where Jetson’s founder and CTO Tomasz Patan, alongside CEO Stephan D’haene, personally oversaw the unboxing and pre-flight preparations.

An experienced aviator, Luckey completed his ground training in under 50 minutes before embarking on his initial low-altitude flights. Jetson attributes this rapid proficiency to Luckey’s extensive background with advanced technologies. CEO Stephan D’haene emphasized the significance of the delivery, stating, “This delivery is more than a milestone—it’s a statement. Launching our first Jetson ONE with Palmer Luckey, a visionary in both consumer and defense technology, sets the tone for Jetson’s commitment to innovation, freedom, and the future of mobility.”

Delivery Process and Product Details

Originally scheduled for early 2023, the delivery experienced delays but was managed with transparency and consistent communication. Tomasz Patan recalled that Luckey valued the updates and encouraged the company to prioritize quality over speed. The handover ceremony concluded with Luckey receiving exclusive Jetson ‘pilot-wings,’ officially recognizing him as a certified Jetson ONE pilot.

This collaboration highlights a shared ambition to advance personal transportation technologies. Jetson is accelerating its rollout, with further deliveries and training sessions planned across the United States and Europe in the coming months. The Jetson ONE Founders Edition, limited to 100 units worldwide, boasts a distinctive two-tone white and carbon design, premium LED lighting, leather upholstery, removable batteries, and a custom instrument cluster. Additional exclusive features include a red swoosh on the fairings, a numbered plaque, and a branded indoor cover, complemented by accessories such as a carbon dolly, extra chargers, and a transport kit.

Industry Context and Future Prospects

Founded in Poland in 2017 and now headquartered in Italy, Jetson has attracted over 500 customers globally. The company’s expansion coincides with rapid technological advancements in robotics and artificial intelligence. Notably, Nvidia’s recent launch of the Jetson Thor supercomputer promises to revolutionize robotics by enabling advanced AI capabilities for real-time inference and reasoning. This development is expected to drive breakthroughs in diverse fields including logistics, surgery, and disaster response, although challenges such as cost and battery life persist.

As the industry evolves, competitors are likely to enhance their AI-powered platforms or seek partnerships with leading AI technology providers, potentially reshaping the competitive landscape. Jetson’s ongoing expansion in the U.S. and integration of cutting-edge AI technologies signal a future where personal aviation could become as accessible as driving, with innovation in both hardware and software defining the next era of mobility.

Thailand’s Nok Air faces international route ban after safety violations

Thailand’s Nok Air Faces International Route Ban Following Safety Violations

Thailand’s Civil Aviation Authority (CAAT) has imposed a suspension on low-cost carrier Nok Air, barring the airline from operating international flights and halting any plans for route expansion. Announced on August 29, 2025, the ban will remain in place until Nok Air addresses a series of safety violations identified during recent inspections, according to reports from The Nation (Thailand).

This regulatory action coincides with an ongoing International Civil Aviation Organization (ICAO) audit of Thailand’s aviation safety system, which is scheduled from August 27 to September 8, 2025. CAAT Director-General Air Chief Marshal Manat Chavanaprayoon emphasized that Nok Air failed to meet the required safety standards. Consequently, the authority has prohibited the airline from operating or expanding both international and domestic routes until it implements corrective measures.

Safety Concerns and Operational Challenges

The CAAT’s investigation uncovered a significant number of safety incidents involving Nok Air between 2023 and 2025. These incidents included engine in-flight shutdowns, runway excursions, hard landings, and tail strikes. Of particular concern were the unresolved engine shutdowns, which the regulator stressed require thorough investigation and risk assessment before the airline can resume normal operations.

In addition to technical issues, the regulator highlighted internal challenges within Nok Air, including a high turnover rate among pilots, flight instructors, and aviation inspectors. CAAT expressed serious concerns about the airline’s organizational safety culture, employee morale, and workforce stability, warning that these factors could undermine operational expertise and overall safety.

“The company has not yet determined the root cause of these incidents or effectively resolved the operational inefficiencies in its flight operations system,” CAAT stated. The authority has granted Nok Air one week to address these issues before reconsidering the suspension.

Market Implications and Industry Reactions

Nok Air’s suspension is poised to alter the competitive dynamics of Thailand’s aviation market. Competitors such as Thai AirAsia and Thai Lion Air are expected to capitalize on the disruption, as passengers increasingly prioritize airlines with stronger safety records. Industry analysts predict that rival carriers will intensify marketing efforts to attract travelers concerned about safety.

Furthermore, the Thai government’s recent initiative to offer free domestic flights to foreign tourists may exacerbate challenges for Nok Air. This program is likely to divert passengers to other airlines, intensifying competition in the domestic market at a time when Nok Air’s international operations remain grounded.

Nok Air’s Response

In response to the suspension, Nok Air CEO Wutthiphum Jurangkool clarified that the airline has not operated international flights since June 2025 but continues to provide domestic services under CAAT’s close supervision. He affirmed that Nok Air complies with maintenance protocols approved by CAAT and international standards and undergoes regular safety audits, including the IATA Operational Safety Audit (IOSA).

As Nok Air endeavors to resolve its safety and operational challenges, the situation will be closely monitored by regulators, competitors, and passengers, with significant implications for Thailand’s broader aviation sector as it strives to meet global safety standards.

Setna iO Acquires Majority Stake in Landing Gear Technologies

Setna iO Acquires Majority Stake in Landing Gear Technologies

Landing Gear Technologies (LGT) has announced the sale of a majority stake to Setna iO, a Chicago-based supplier of aircraft parts. This strategic transaction aims to accelerate LGT’s growth while preserving its core values and operational standards. The acquisition is intended to strengthen LGT’s market position and expand its capabilities, as Setna iO seeks to enhance its maintenance, repair, and overhaul (MRO) and component supply businesses.

Leadership Continuity and Strategic Vision

Under the new ownership structure, Raul and Ibis Cruz-Alvarez, alongside Roly Estrada, will retain significant ownership and continue to lead LGT. This continuity is designed to maintain the company’s reputation for customer service, quality, and timely delivery. Raul Cruz-Alvarez, CEO of LGT, emphasized the benefits of the partnership, stating that it will provide the necessary resources to expand capabilities and introduce new platforms, all while upholding the company’s commitment to its partners and team. He affirmed that his family remains fully dedicated to leading LGT and sustaining its trusted industry standing.

David Chaimovitz, CEO of Setna iO, highlighted the strategic alignment of the acquisition. He noted that integrating LGT’s team and services will enable Setna iO to offer more comprehensive, top-level in-house MRO services, thereby delivering a streamlined solution to customers. Chaimovitz expressed optimism about the partnership and the value it is expected to generate.

Operational Integration and Industry Challenges

LGT’s management team and existing employees will remain in place following the acquisition, with plans to expand the workforce to support new product lines and services in the near future. The transition is not anticipated to disrupt existing contracts or ongoing business operations.

However, the acquisition occurs amid increased scrutiny of the landing gear sector. Recent incidents, including an F-35 crash linked to contaminated landing gear fluid, have heightened regulatory attention and raised concerns about safety and quality control within the industry. Both Setna iO and LGT will need to navigate these challenges carefully to maintain market confidence and ensure a seamless operational integration.

Market reactions to the deal may include investor skepticism regarding the strategic fit and the realization of operational synergies. Competitors might respond by pursuing their own partnerships in landing gear technology or adopting aggressive pricing strategies to protect their market share.

Despite these potential obstacles, both companies express confidence in their ability to build on LGT’s strong foundation and enhance services for a global customer base. The combined resources and expertise are expected to position the company for sustained growth and innovation in the evolving aerospace sector.

Singapore Plans Investment in Indian Civil Aviation MRO Facilities: MEA

Singapore Plans Investment in Indian Civil Aviation MRO Facilities: MEA

Strengthening Bilateral Cooperation in Civil Aviation

Singapore is actively pursuing deeper collaboration with India by investing in the development of maintenance, repair, and overhaul (MRO) capabilities within India’s civil aviation sector, according to P Kumaran, Secretary (East) at India’s Ministry of External Affairs. Speaking during a special briefing coinciding with Singapore Prime Minister Lawrence Wong’s official visit to India, Kumaran identified civil aviation as a pivotal area of bilateral engagement. He emphasized that cooperation extends beyond increasing connectivity and flight frequencies to include the strategic development of MRO infrastructure, describing it as a “very promising area” for partnership.

Singapore’s expertise in MRO is well established, and the country aims to leverage this strength by investing in Indian facilities to enhance capacity. A key player in this initiative is SIA Engineering Company Limited, a Singapore-based aircraft maintenance specialist. The company is reportedly exploring a partnership with India’s Tata Group, a collaboration that aligns with Singapore Airlines’ 25 percent stake in Air India. Kumaran noted that this partnership would capitalize on India’s ample land availability to establish new MRO facilities, thereby creating synergies between the two nations’ aviation sectors.

Challenges and Market Dynamics

Despite the promising outlook, expanding MRO cooperation faces several challenges. Regulatory approvals remain a significant hurdle, alongside competition from established MRO providers within India. The sector also requires a skilled workforce to meet growing demands. The Indian MRO market is currently undergoing consolidation, exemplified by the Adani Group’s acquisition of AAR-Indamer Technics. Such developments may influence Singapore’s investment approach and prompt existing players to forge new alliances or expand operations to safeguard their market positions.

Broader Framework of India-Singapore Collaboration

Prime Minister Wong’s visit saw the signing of five key Memoranda of Understanding (MoUs) between India and Singapore, covering a range of strategic sectors. These agreements include initiatives on a green and digital shipping corridor, space sector collaboration, civil aviation training and research, digital asset innovation, and the establishment of a national centre of excellence for advanced manufacturing skills in Chennai.

This latest round of agreements builds on prior cooperation, such as the semiconductor ecosystem partnership MoU signed during Prime Minister Narendra Modi’s visit to Singapore last year. That agreement has fostered a bilateral semiconductor policy dialogue focused on investment, business linkages, skill development, and research and development to bolster India’s semiconductor industry.

The green and digital shipping corridor MoU aims to promote collaboration on zero-emission fuel supply chains, benefiting maritime industries in both countries. The digital asset innovation agreement will enhance cooperation between the Reserve Bank of India and the Monetary Authority of Singapore, particularly in the development of central bank digital currencies. Furthermore, India’s space agency ISRO, which has previously launched 18 Singaporean satellites, is expected to deepen its partnership with Singapore under the new space sector agreements.

As India and Singapore expand their cooperation across multiple domains, the focus on MRO investment highlights the strengthening strategic and economic ties between the two countries, while also reflecting the evolving competitive landscape within India’s aviation industry.

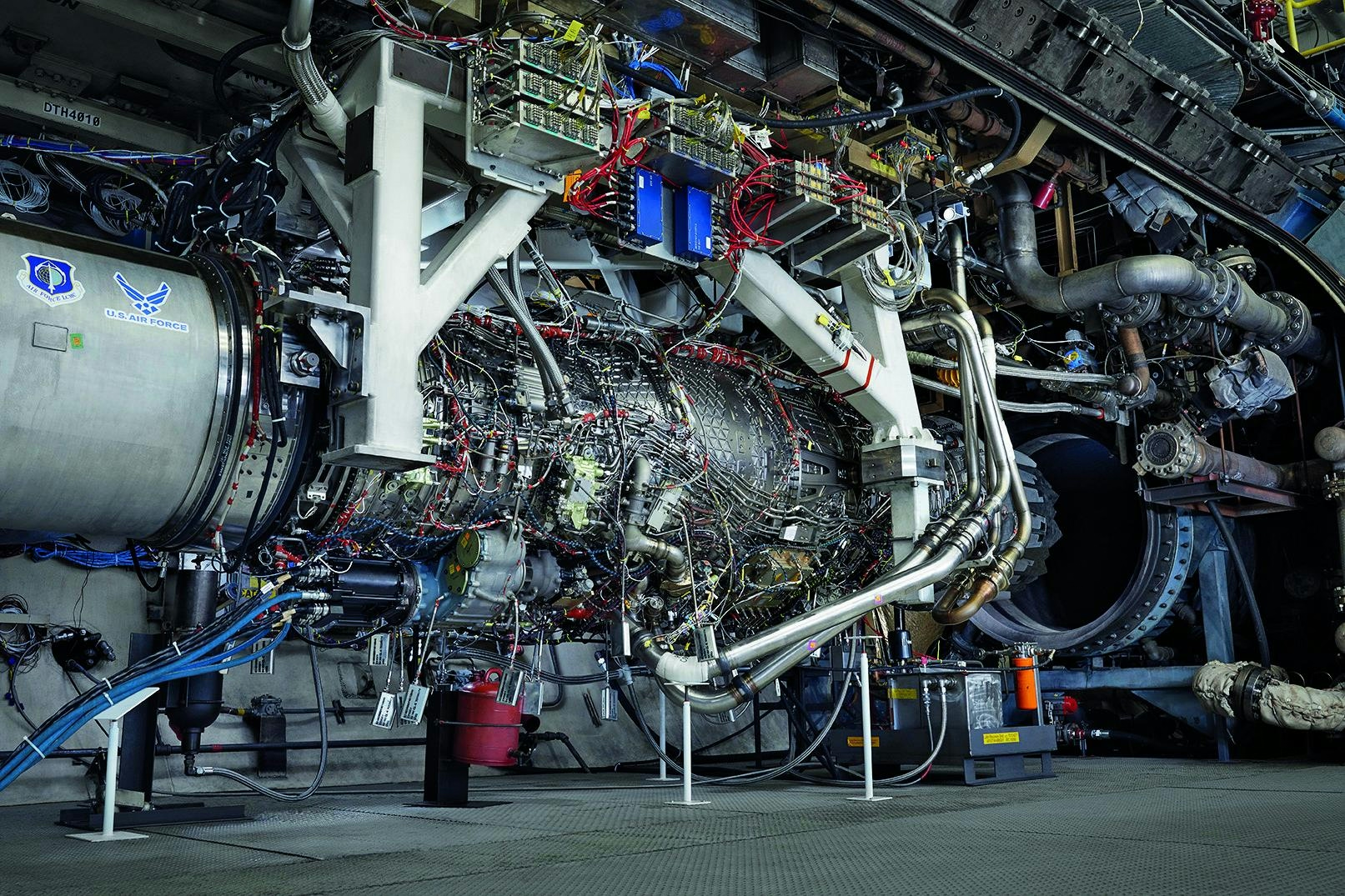

GE Aerospace Partners to Develop Hybrid Electric Aircraft Engines

GE Aerospace and BETA Technologies Collaborate on Hybrid Electric Aircraft Engines

GE Aerospace has entered into a strategic partnership with BETA Technologies, committing $300 million to accelerate the development of hybrid electric aircraft engines. This collaboration seeks to advance gas-electric propulsion systems for both defense and commercial aviation sectors, representing a significant move toward more sustainable air travel solutions.

Advancing Hybrid Propulsion Technology

As a dominant supplier of jet engines, powering approximately 75% of commercial aircraft worldwide, GE Aerospace is broadening its technological focus to include electric and hybrid gas-electric engines. BETA Technologies, based in Vermont and specializing in electric aircraft and propulsion systems, brings expertise that is expected to drive innovation in hybrid engine technology. The partnership aims to enhance the range and speed capabilities of smaller aircraft, particularly those used in cargo and supply missions within defense applications.

Despite the promising outlook, the development of hybrid electric flight faces considerable challenges. The collaboration must address regulatory complexities, ensure seamless integration of new propulsion technologies with existing aircraft systems, and develop the necessary infrastructure to support electric aviation. Industry experts highlight that current electric and hybrid engines are primarily suited for short-haul routes, such as those operated by air taxis, and emphasize that substantial improvements in battery technology remain essential before electric propulsion can supplant traditional jet fuel on longer flights.

Market Response and Industry Implications

The market has reacted positively to GE Aerospace’s investment in BETA Technologies, interpreting it as a strong endorsement of the future potential of electric aviation. This strategic move is likely to encourage competitors to intensify their research and development efforts or pursue new partnerships to maintain competitiveness in this rapidly evolving sector.

GE Aerospace’s commitment to innovation is evident in its 2024 research and development budget, which has reached $1.3 billion, accounting for nearly 4% of its annual sales. The company’s stock has experienced a 69% increase this year, driven by investor confidence in its strategic direction and technological progress.

Wall Street analysts remain optimistic, with all 12 analysts covering GE Aerospace in the past three months issuing Buy ratings. The consensus price target stands at $300.33, indicating a potential upside of nearly 7% from current trading levels.

As GE Aerospace and BETA Technologies continue to navigate technical and regulatory hurdles, their partnership highlights the growing momentum behind hybrid electric propulsion and the broader industry push toward sustainability in aviation.

Why Emirates Operates Without Narrowbody Aircraft

Why Emirates Operates Without Narrowbody Aircraft

Emirates distinguishes itself in the global aviation sector as the largest airline operating an exclusively widebody fleet, deliberately excluding narrowbody aircraft from its operations. This strategic choice is deeply influenced by the airline’s geographic positioning in the Middle East, its reliance on a hub-and-spoke operational model, and a concentrated emphasis on efficiency and profitability through the deployment of large, long-range jets.

The World’s Largest Widebody Fleet

Emirates commands a fleet of 261 widebody aircraft, comprising the world’s largest assemblages of Airbus A380s and Boeing 777s. This fleet size significantly surpasses that of its nearest competitors. For instance, United Airlines, which holds the second-largest widebody fleet, operates approximately 226 aircraft, many of which are smaller models such as the Boeing 767 and 787. Emirates’ dedication to widebody aircraft is further demonstrated by its substantial order of 204 Boeing 777X jets, positioning the airline to maintain its status as the foremost operator of these advanced next-generation aircraft.

While other carriers, including Virgin Atlantic, also maintain all-widebody fleets, their scale is comparatively modest. Virgin Atlantic’s fleet consists of just 44 aircraft, and other all-widebody operators like Air Tahiti Nui operate even fewer. Among Gulf carriers, Qatar Airways and Etihad Airways maintain significant widebody fleets as well, but neither approaches the size or scope of Emirates’ operations.

Hub-and-Spoke Model at a Global Crossroads

The sustainability of Emirates’ all-widebody fleet is closely tied to its hub-and-spoke model, centered at Dubai International Airport. This model channels passengers from across Asia, the Pacific, Africa, and Europe through a single, strategically located hub. Emirates’ long-range aircraft facilitate connections between distant markets, including North America and parts of South America, enabling high-capacity flights that optimize both efficiency and profitability.

In contrast to many global airlines that have shifted toward more flexible point-to-point networks, Emirates remains steadfast in its commitment to the hub-and-spoke system. This approach allows the airline to consistently fill large aircraft, thereby justifying the deployment of widebodies on nearly all routes.

Strategic Focus and Market Challenges

Emirates’ choice to exclude narrowbody aircraft is also shaped by the presence of flydubai, Dubai’s other major airline, which specializes in regional and short-haul routes using narrowbody jets. This clear division of labor permits Emirates to focus exclusively on long-haul, high-density markets where widebody aircraft are most effective.

Nevertheless, this strategy presents challenges. Emirates continues to grapple with Boeing’s production delays and global supply chain disruptions, which have hindered the delivery of new aircraft and affected fleet expansion plans. Additionally, the airline has expressed concerns regarding protectionist policies in key markets such as India, arguing that such regulations impede its growth and restrict access to lucrative routes.

Competitive Landscape

By not operating narrowbody aircraft, Emirates leaves room for competitors to serve regional and secondary markets. Rival airlines often leverage mixed fleets to address these segments, particularly where Emirates’ widebody-only approach is less practical.

Despite these challenges, Emirates’ unwavering focus on widebody aircraft remains central to its corporate identity and operational success, enabling it to dominate long-haul travel and sustain its position as a global leader in aviation.

B&H Worldwide Delivers Airbus H145 Helicopter to New Zealand for GCH Aviation

B&H Worldwide Delivers Airbus H145 Helicopter to New Zealand for GCH Aviation

B&H Worldwide has completed the transportation of an Airbus H145 helicopter from Zurich, Switzerland, to Auckland, New Zealand, on behalf of GCH Aviation. This delivery marks a pivotal advancement in expanding air rescue and emergency medical services across New Zealand. It is the first of four H145 helicopters scheduled for arrival in 2025, as part of GCH Aviation’s strategic investment to enhance operations in the Canterbury, West Coast, Nelson, and Marlborough regions.

Complex Logistics and International Coordination

The operation involved a highly complex logistics process, requiring B&H Worldwide to devise a bespoke international transport solution. This included custom crating, meticulous global freight coordination, and strict compliance with New Zealand’s stringent biosecurity and aviation regulations. The helicopter’s route, which passed through Frankfurt, Hong Kong, and Melbourne aboard a Boeing 747 freighter, demanded precise planning to meet local operational standards and ensure timely delivery.

B&H Worldwide’s team conducted extensive evaluations of multiple routing options and collaborated closely with airline partners to secure the most efficient and reliable transport solution. Lee Hedges, Branch Manager for New Zealand at B&H Worldwide, emphasized the company’s expertise in managing specialised aerospace movements. He noted that by overseeing the complex logistics, B&H Worldwide enabled GCH Aviation to concentrate on the technical preparation and reassembly of the helicopter.

Strategic Importance and Market Context

Declan Smiddy, CEO of GCH Aviation, underscored the significance of the delivery, describing the arrival of the H145 as a major step forward in strengthening New Zealand’s air rescue and emergency medical capabilities. He praised B&H Worldwide for their efficiency and expertise, which ensured the helicopter’s smooth transit from Europe to the local facility.

This delivery occurs amid increasing competition within New Zealand’s helicopter market. The country is concurrently acquiring MH-60R naval warfare helicopters from Sikorsky, prompting manufacturers to enhance their offerings to meet evolving operational demands. Furthermore, advancements in autonomous helicopter technology, exemplified by Airbus’s collaboration with Shield AI, are influencing market dynamics and shaping future procurement strategies.

Stuart Allen, Group CEO of B&H Worldwide, who was present in Auckland during part of the helicopter’s reassembly, highlighted the strategic role his company plays in supporting the aerospace sector. He remarked that being on-site alongside partners reflects B&H Worldwide’s commitment to customer success at every organisational level. Allen described the delivery as a prime example of the company’s ability to work closely with customers to deliver mission-critical aerospace assets reliably and safely.

Alongside the four H145 helicopters, GCH Aviation anticipates the arrival of additional aircraft and a flight simulator later this year. This successful delivery further demonstrates B&H Worldwide’s growing expertise in rotary-wing logistics, providing end-to-end solutions for high-value, mission-critical aerospace assets within a competitive and rapidly evolving market.

Delays at Airbus and Boeing Raise Concerns Over Air Cargo Capacity

Delays at Airbus and Boeing Raise Concerns Over Air Cargo Capacity

Major air cargo operators are increasingly warning of an impending capacity shortage as aging fleets and delivery delays from Boeing and Airbus threaten to constrain the global supply of large freighter aircraft. Michael Steen, CEO of US-based Atlas Air, highlighted that the imbalance between supply and demand for wide-body freighters is expected to worsen in the coming years.

Factors Driving the Capacity Shortfall

Steen attributes the growing shortfall to several converging factors: a wave of aircraft retirements, limited new capacity entering the market, and ongoing supply chain challenges affecting aircraft manufacturers. Of the approximately 630 large wide-body freighters currently in service worldwide, up to 150 have reached or exceeded the typical retirement age of 25 years. This aging fleet presents a significant challenge to maintaining adequate air cargo capacity.

Aircraft remain vital to global trade, transporting roughly one-third of goods by value—an estimated $8.3 trillion annually, according to the International Air Transport Association. The surge in e-commerce and increased shipments from Asia to Western markets have further intensified demand for air cargo services in recent years.

Production Delays and Market Implications

Despite rising demand, deliveries of new wide-body freighters remain constrained. Both Boeing and Airbus continue to grapple with material shortages and labor constraints that have delayed production schedules. Frank Bauer, chief operating officer at Lufthansa Cargo, described these delivery delays as a “key constraint” for the sector.

Boeing currently faces a backlog of 63 wide-body 777 freighter orders, according to aviation advisory firm IBA. The manufacturer is producing four 777 and 777-9 aircraft per month, but the first deliveries of its next-generation 777-8F cargo aircraft, which began production in July, have been postponed from 2027 to 2028. Airbus has similarly delayed the introduction of its A350 freighter from 2026 to the second half of 2027 due to persistent supply chain issues.

These delays are influencing market dynamics. Boeing’s share price has risen sharply, buoyed by the prospect of a significant 500-aircraft deal with China that could reverse a seven-year slump in deliveries to the country. Meanwhile, Airbus, despite its own supply chain challenges, has maintained more predictable delivery schedules. In July 2025, Airbus delivered eight wide-body aircraft compared to Boeing’s ten and is expected to surpass Boeing in narrow-body deliveries. These shifts may reshape the competitive landscape and further impact air cargo capacity.

Industry Response and Future Outlook

Airlines are now urgently seeking to secure freight capacity amid these constraints. Loay Mashabi, CEO of Saudia Cargo, warned of a challenging period ahead, stating, “There will be a few years of challenge... it will hit us severely before we know it.” Some operators are attempting to extend the service life of aircraft beyond 30 years, but Mashabi cautioned that rising maintenance and fuel costs are making this approach increasingly prohibitive.

Analysts suggest that tightening global air cargo capacity could enhance operators’ pricing power and drive up freight rates. However, ongoing geopolitical uncertainties—including Houthi attacks on Red Sea shipping lanes and unpredictable US trade policies—continue to cloud demand forecasts.

Boeing declined to comment on these developments, while Airbus did not respond to requests for comment.

Beonic Introduces AI-Powered LiDAR Technology at Queenstown Airport

Beonic Introduces AI-Powered LiDAR Technology at Queenstown Airport

Queenstown Airport has embarked on a significant technological advancement by implementing Beonic’s AI-powered LiDAR system, designed to optimize passenger flow and improve operational efficiency. With global passenger volumes steadily increasing, airports are under growing pressure to manage congestion, minimize wait times, and provide a seamless travel experience. Queenstown’s adoption of this innovative technology positions it as a leader in New Zealand’s aviation sector.

Enhancing Passenger Management Through AI and LiDAR

The newly deployed AI-driven LiDAR (Light Detection and Ranging) system is now active across five departure zones within the terminal. Unlike conventional monitoring methods, Beonic’s solution does not collect personal data. Instead, it employs laser pulses to generate a three-dimensional digital model of the terminal environment, enabling staff to monitor queue lengths, occupancy rates, and potential congestion points while safeguarding passenger privacy.

The system’s artificial intelligence analyzes movement patterns to anticipate crowding before it occurs. For example, when multiple flights are scheduled to depart in close succession, the technology can alert airport personnel to allocate additional resources or open extra counters proactively. This predictive functionality is particularly valuable during peak travel periods or unforeseen disruptions, facilitating smoother passenger journeys.

Improving Passenger Experience with Real-Time Information

Although the primary objective is to enhance operational workflows, passengers stand to gain significantly from the system’s capabilities. Real-time data on wait times can be communicated through digital signage, mobile applications, or public announcements, providing travelers with timely and accurate updates. This transparency helps alleviate common frustrations associated with long queues and inadequate communication, thereby reducing travel-related stress.

Positioning Amidst a Competitive AI Landscape

Beonic’s introduction of AI-powered LiDAR at Queenstown Airport occurs within a rapidly evolving technological environment marked by intense competition. Established companies such as Waymo, which integrates LiDAR and radar for autonomous vehicles, and Tesla, which relies on camera-based systems, represent significant players in the sensor technology market. Beyond aviation, the broader AI sector is witnessing mixed responses to new tools, exemplified by Google’s financial AI offerings and the varied reception to OpenAI’s GPT-5.

Competitors are likely to respond by advancing their own AI capabilities or adopting similar technologies to maintain market relevance. Meanwhile, Queenstown Airport’s robust financial performance and commitment to ongoing investment create a conducive atmosphere for innovation, enhancing the prospects for successful technology integration.

Future Implications for Aviation Technology

By harnessing AI-powered LiDAR, Queenstown Airport is not only advancing its operational efficiency but also establishing a benchmark for passenger experience within New Zealand. As the aviation industry continues to evolve in response to shifting demands and technological progress, this initiative may serve as a catalyst for wider adoption of AI-driven solutions across airports globally.

Airlines Confront Rising Labor Costs Amid Growing Use of AI

Airlines Confront Rising Labor Costs Amid Growing Use of AI

The airline industry is grappling with escalating financial pressures as rising labor costs intersect with operational challenges and the accelerated integration of artificial intelligence (AI). Between 2023 and 2025, wages for pilots and flight attendants have increased by 8 to 15 percent, while ground staff salaries have risen by 6.2 percent year-over-year. This surge is driven by fierce competition for talent amid persistent staffing shortages. According to the International Air Transport Association (IATA), total labor costs are projected to reach $253 billion in 2025, marking a 7.6 percent increase from 2024. Despite productivity improvements that have limited average labor unit cost increases to just 0.5 percent, airlines face a difficult balancing act between managing rising expenses and maintaining operational efficiency.

Industry-Specific Pressures Intensify

In addition to wage inflation, airlines confront a range of sector-specific challenges that compound financial strain. Supply chain disruptions have delayed the delivery of new aircraft, compelling carriers to rely on aging fleets that demand more maintenance and offer reduced fuel efficiency. The growing threat of cyberattacks has necessitated increased investment in digital infrastructure and security measures. Regulatory requirements for Sustainable Aviation Fuel (SAF) introduce further complexity, requiring costly training and compliance efforts. Geopolitical instability has also contributed to rising insurance premiums and forced airlines to undertake expensive rerouting around conflict zones. Recent labor disputes, such as the Air Canada strike, underscore the potential for significant operational disruptions and sudden cost escalations.

AI and Automation: A Strategic Response

In response to these mounting pressures, airlines are rapidly expanding their use of AI and automation technologies. AI-powered systems are being deployed to optimize crew scheduling, reduce aircraft turnaround times, and streamline baggage handling, thereby minimizing delays and lowering operating costs. Generative AI facilitates dynamic workforce planning by aligning staffing levels with real-time demand, reducing instances of overstaffing or understaffing. Automation of repetitive tasks allows frontline employees to concentrate on customer service and operational efficiency. Alaska Airlines’ “Alaska Inspires” platform, which employs generative AI to enhance booking rates, exemplifies how technology can simultaneously drive revenue growth and address labor constraints.

Competitive and Market Implications

The airline industry’s adoption of AI reflects broader trends across labor-intensive sectors. In hospitality, AI-driven solutions have halved room turnaround times and achieved task completion rates as high as 99 percent in some hotels. Manufacturing is similarly increasing AI integration to mitigate labor shortages and bolster cybersecurity, although high implementation costs and supply chain challenges persist. As airlines and their competitors increasingly rely on AI to streamline operations and reduce dependence on human labor, market consequences may include higher ticket prices and pressure on profit margins. Workforce reductions and substantial investments in employee reskilling are anticipated, raising concerns about widening income inequality.

Profitability Gains and Ongoing Risks

AI-driven initiatives are already yielding measurable financial benefits for airlines. Those employing AI for dynamic pricing have reported revenue increases ranging from 12 to 18 percent, while predictive maintenance has reduced aircraft downtime by 35 percent and cut maintenance expenses by 25 percent. Delta Air Lines, for example, is piloting AI-based dynamic pricing on 20 percent of its flights to optimize fares in real time. Nevertheless, significant risks remain. Automation threatens routine jobs, and only a small fraction of companies—approximately 1 percent—consider themselves fully mature in AI deployment, highlighting gaps in technological readiness.

As labor costs continue to rise and operational complexities deepen, airlines are placing considerable bets on AI to protect profitability. However, the sector must carefully navigate the twin challenges of workforce disruption and the ongoing need for investment in both human capital and technological infrastructure.

New Autonomous Air Taxi Can Carry Passengers Hundreds of Miles Without a Pilot

EHang Advances Autonomous Air Taxi Technology with Long-Range VT35 Model

China’s EHang is rapidly emerging as a key player in the global electric vertical takeoff and landing (eVTOL) market, pushing the boundaries of autonomous air mobility. In 2023, the company’s two-seat EH216-S became the first electric air taxi to receive certification from Chinese authorities, enabling its commercial deployment in local tourism sectors. Following certification, EHang commenced large-scale production and initiated limited tourism flights in cities such as Guangzhou and Hefei, signaling a significant step toward mainstream adoption.

Expanding Horizons in China’s Low-Altitude Economy